More than 32.7 million residential properties from Texas to Maine are at risk of moderate or severe damage sustained from hurricane-force winds, a new report shows.

The large number of at-risk homes in CoreLogic’s 2024 Hurricane Risk Report, which comes as an ominous 2024 Atlantic hurricane season approaches, equates to a combined reconstruction cost of $10.8 trillion.

The hurricane season is widely expected to be an active one.

The National Oceanic and Atmospheric Administration is predicting an 85% chance of an above-average Atlantic hurricane season, with up to 25 named storms. Colorado State University’s forecasting team in April called for 23 named storms, 11 hurricanes and five major hurricanes. Accuweather meteorologists in March also forecast an above-average Atlantic hurricane season with as many as 20 to 25 named storms.

In addition to properties exposed to high wind, CoreLogic said roughly 7.7 million properties with a combined reconstruction cost value (RCV) of $2.3 trillion have direct or indirect coastal exposure, which makes them susceptible to storm surge—not covered by standard homeowners insurance policies.

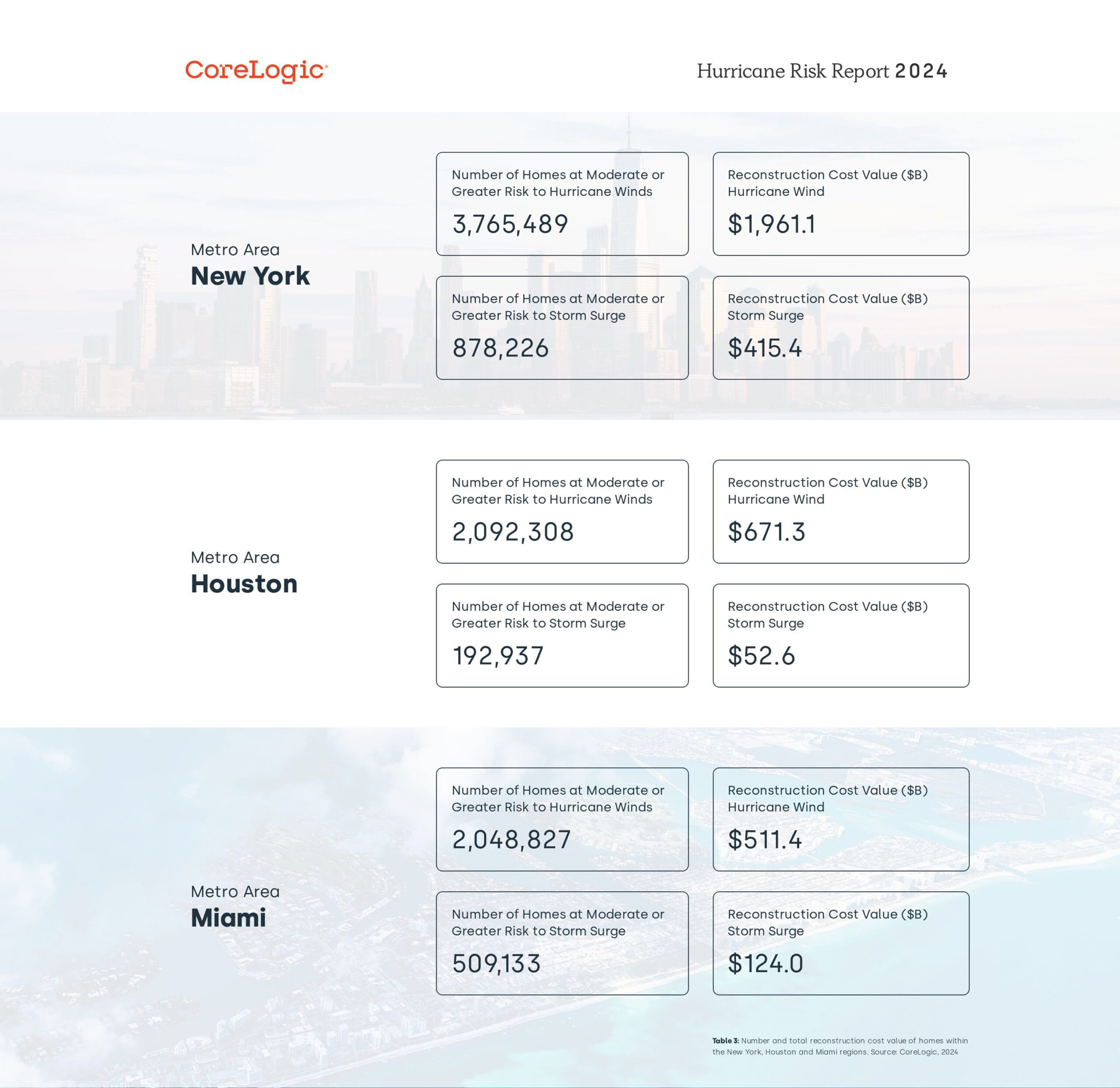

To contextualize the risk, the report focuses on three metro areas: New York, Houston and Miami.

“Miami, New York and Houston are densely populated metropolitan areas with extensive urban infrastructure,” CoreLogic said in the report. “The concentration of people, buildings, and critical infrastructure increases the potential for widespread damage and disruption in the event of a hurricane. Storm surge poses a significant threat to coastal cities like Miami and New York, where densely populated areas are situated near the coastline. Additionally, Houston’s sprawling urban landscape, coupled with its susceptibility to flooding, heightens the risk of hurricane-related impacts on the city’s infrastructure and residents.”

More than 3.7 million homes in New York with a RCV of about $2 trillion are at “moderate or greater risk” from hurricane winds, and 878,226 homes are at risk from storm surge with a reconstruction cost of $415.4 million, according to the report (chart above with similar numbers for Houston and Miami).

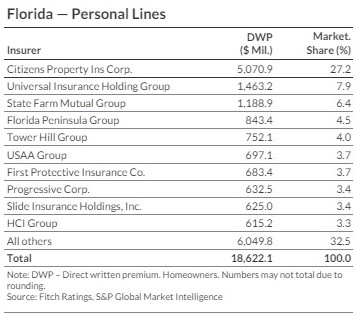

In its annual report on hurricane exposure out this week, Fitch Ratings said a Florida hurricane landfall with substantial damage could be a problem for more thinly capitalized individual homeowner specialists, but that the industry’s capital strength provides overall support to withstand a significant hurricane event in 2024. That report also points out the potential effects of state regulatory and legislative changes intended to help the market, which remain to be seen.

“The Florida insurance market is still adapting to significant regulatory and legislative changes enacted from 2021 to 2023,” Fitch said. “The magnitude of loss cost declines from changes in the volume of litigated claims, assignment of benefits (AOB) reforms, and reducing fraud is uncertain, but signs of new capacity entering the market are more evident.”

Policies in force at Florida’s state-sponsored Citizens Property Insurance Corporation—the largest insurer of personal lines in the Sunshine State—peaked around September 2023 at about 1.4 million, but have fallen to 1.2 million as of May. Fitch said it anticipates that policy count will continue to decline in the near term as more carriers take an interest in policy take-outs. Pricing on reinsurance renewals at the June/July midyear mark are moderating, with risk-adjusted rates generally flat to down slightly, according to the report.

Policies in force at Florida’s state-sponsored Citizens Property Insurance Corporation—the largest insurer of personal lines in the Sunshine State—peaked around September 2023 at about 1.4 million, but have fallen to 1.2 million as of May. Fitch said it anticipates that policy count will continue to decline in the near term as more carriers take an interest in policy take-outs. Pricing on reinsurance renewals at the June/July midyear mark are moderating, with risk-adjusted rates generally flat to down slightly, according to the report.

“This is in contrast to the 2023 renewals, when Florida property experienced 30%-40% rate rises for catastrophe loss hit business, reflecting the impact of Hurricane Ian in 2022,” the report states. “Terms and conditions are holding firm, with retentions steady and not returning to levels that provide earnings protection to cedents.”

Tal Paschal, a product manager for CoreLogic, said the greatest concern is the potential of hurricanes to not only make landfall but to hit populated areas.

“[2020’s Hurricane] Laura hit Southwest Louisiana,” Paschal said. “If it would have gone 200 miles to the east, it could have hit New Orleans, if it would have gone 150 miles West, it could have hit Houston. So, I think like it’s important to remember that hurricane activity varies from year to year and nothing is certain.”

If the season unfolds as feared, it would mean a second consecutive year with far above the average number of hurricanes. The 2023 season produced 20 named storms, the fourth-highest amount on records, which included 10 hurricanes. The average is 14 named storms per season from 1990 to 2021, according to CoreLogic.

Despite 2023’s active season, the report shows that only one Atlantic storm made landfall in the U.S. as a hurricane. Hurricane Idalia hit in remote part of the Florida coastline. CoreLogic estimates insured losses across the southeastern U.S. from Idalia to be less than $2 billion.

Julie Serakos, managing director of insurance for Moody’s, on Wednesday issued a commentary on the season’s outlook, calling attention to the losses that have piled up the past few years.

“North Atlantic Hurricanes have cost the insurance industry $275 billion in insured losses since 2017, when the 12-year hurricane drought ended,” Serakos wrote. “Event losses are escalating due to population increases in coastal areas, social inflation, construction inflation, and regulatory mandates.”

Photo: Rows of homes damaged by Hurricane Andrew in 1992. (AP Photo/Mark Foley, File)

Topics Catastrophe Natural Disasters Florida New York Hurricane

Was this article valuable?

Here are more articles you may enjoy.

‘Structural Shift’ Occurring in California Surplus Lines

‘Structural Shift’ Occurring in California Surplus Lines  The $10 Trillion Fight: Modeling a US-China War Over Taiwan

The $10 Trillion Fight: Modeling a US-China War Over Taiwan  Trump’s EPA Rollbacks Will Reverberate for ‘Decades’

Trump’s EPA Rollbacks Will Reverberate for ‘Decades’  AIG’s Zaffino: Outcomes From AI Use Went From ‘Aspirational’ to ‘Beyond Expectations’

AIG’s Zaffino: Outcomes From AI Use Went From ‘Aspirational’ to ‘Beyond Expectations’