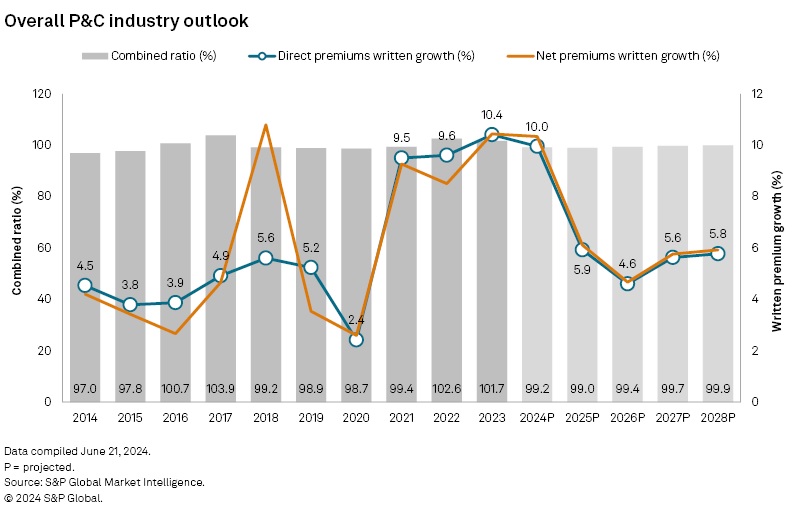

S&P Global Market Intelligence is forecasting a combined ratio of 99.2 for the U.S. P/C insurance industry overall in 2024, signifying a return to underwriting profitability for the first time since 2021.

According to the analysis, private passenger auto insurance is expected “to make a dramatic return to underwriting profitability,” with S&P GMI projecting a personal auto 2024 combined ratio of 98.4, down from 104.9 in 2023 and 112.2 in 2022. With personal auto representing almost 35 percent of overall P/C insurance industry premiums written, that turnaround is what will drive the overall underwriting profit for the industry, according to S&P GMI projections presented in the “S&P Global Market Intelligence 2024 U.S. P&C Insurance Market Report” published late last week.

The combined ratio for the industry overall will drop 2.5 points to 99.2 from a level of 101.7 in 2023, and improve a bit more to 99.0 in 2025, the report shows.

S&P GMI’s forecast that industrywide underwriting results will be back in the black this year contrasts projections from analysts at the Insurance Information Institute and Milliman. They indicate that the industry will record another overall underwriting loss—and an underwriting loss in the personal auto line—in 2024, with recovery not anticipated until 2025.

Related: P/C Premium Growth Likely But Profits Delayed Until 2025: Forecast

With homeowners results lagging behind personal auto, S&P GMI is not anticipating that the personal lines segment overall will record an underwriting profit this year or next year. The personal lines combined ratio will come close to breakeven in 2026, according to the five-year projections provided by line and segment in the report. The projected personal lines combined ratios are 101.2 for 2024 and 100.2 for 2025, compared to 106.7 in 2023.

Weather catastrophes continue to weigh on the homeowners business, and although the report notes (in a section outlining the methodology) that S&P GMI assumes a normal catastrophe load for exposed business lines, for homeowners, the combined ratio is still pegged at an unfavorable 107.3 for 2024. That’s down from 110.9 in 2023, which had been the worst result in a dozen years.

For personal lines insurers, results will also continue to be uneven as mutuals and reciprocals need more than rate hikes to recover from challenges to auto and homeowners lines in recent years, the report says. (Discussed further below.)

The commercial lines segment will remain profitable throughout the five-year projection period, although charts in the report reveal that the projected 2024 commercial lines combined ratio of 96.0 will creep up to 98.2 by 2028.

The highest combined ratio projection for the U.S. P/C insurance industry overall is also indicated for the last year of the forecast period—99.9 for 2028—with underwriting results remaining in the black throughout the five-year time frame.

The report calls out a “faster-than-expected erosion” in workers compensation results as the most significant risk to S&P GMI’s commercial lines outlook for continued underwriting profitability.

Commenting on drivers of earnings beyond underwriting profit, the S&P GMI report notes that “the industry stands to benefit materially from higher interest rates” after years and years of net yields on invested assets coming in at record low levels.

“The industry’s ongoing effort to rotate into high-quality, higher-yielding assets will serve as a catalyst for growth in net income even to the extent that underwriting margins remain relatively modest,” the report says.

“A key variable will be the industry’s continued adherence to disciplined underwriting in a more forgiving investment landscape,” the report says.

Top Line Growth Set to Drop

On the top line, S&P GMI projects a final year of double-digit industrywide growth in 2024, with premiums across all lines jumping 10 percent for full-year 2024 but then falling to 5.9 percent or lower in 2025-2028.

“A substantial decline in the pace of increases in private auto premium volumes serves as the primary contributor to our projection that the rate of growth in U.S. P/C industry direct premiums written will recede to the mid-single digits on an annual basis from 2025 through 2028,” said Tim Zawacki, insurance sector strategist at S&P Global Market Intelligence in a statement accompanying the report. Zawacki explained that the magnitude of the improvement in underwriting results is likely to prompt “fairly rapid retreats in the scope and scale” of the significant personal auto rate increases pursued by most market participants over the last three years.

According to the report, S&P GMI’s RateWatch application showed aggregate approved rate changes through the first half of 2024 dropping to 5.9 percent, down from an “outsized full-year 2023 tally” of 15.2 percent. Still, the rate hikes taking effect in the second half of 2023 have yet to fully impact income statements through 2024, the report notes, adding that rate momentum has persisted in the other major personal line: homeowners.

While the report shows direct premium growth for all personal lines hovering around 14 percent for 2023 and 2024, and dropping to the 4-7 percent range in the subsequent five years, commercial lines growth rates have already fallen below double-digit levels of 2021 and 2022. The projected commercial lines direct premium growth rate is 6.2 percent for 2024, with growth rates thereafter in the 5-6 percent range.

Overall, the 10 percent growth in direct premiums written across all lines marks the fourth straight year for growth of 9.5 percent or more.

“The duration of the expansion is without precedent in at least a generation as the previous comparable hard-market cycle in the early part of the 21st Century had only three years with annual growth rates of 9.5 percent or more,” the report notes.

Relative Performance

The report includes line-by-line details for historical combined ratio and growth rates going back to 2014 and projected forward to 2028, along with aggregations for the personal and commercial lines sector and the U.S. P/C insurance industry. For each line analyzed and for the segments, the report also presents charts displaying combined ratios and premiums for the top 15 players.

In private passenger auto, for example, the report shows that only Erie (ranked 12th by 2023 premium) and CSAA (ranked 14th) posted worse combined ratios than the biggest personal auto insurer, State Farm, in 2023. State Farm’s 115.3 combined ratio towered over the ratios recorded for the second- and third-largest writers—Progressive and GEICO, coming in at 94.2 and 92.1, respectively. Erie Insurance posted a 123.3 ratio and CSAA’s result was 117.1, according to S&P GMI.

The report includes a section devoted to S&P GMI’s performance rankings—determined by S&P GMI analysts using 13 financial metrics from 2023 statutory filings to measure rates of return, balance sheet expansion, investment performance and prior-accident-year reserve development, in addition to underwriting profitability and premium growth. Commercial lines players dominate those rankings, but balance could return, with tailwinds benefiting personal lines carriers while headwinds are already emerging in certain parts of the commercial lines, Zawacki observed in a recent article he wrote about the rankings for Carrier Management.

Analyzing relative premium growth rates for individual carriers, S&P GMI shows that Tesla Insurance was the biggest sprinter with a triple-digit growth rate of nearly 768 percent putting direct and net written premiums at roughly $110 million.

Related article: Tesla Insurance Blasts Off to Top P/C Insurance Growers Chart

Personal v. Commercial; Stock vs. Mutual

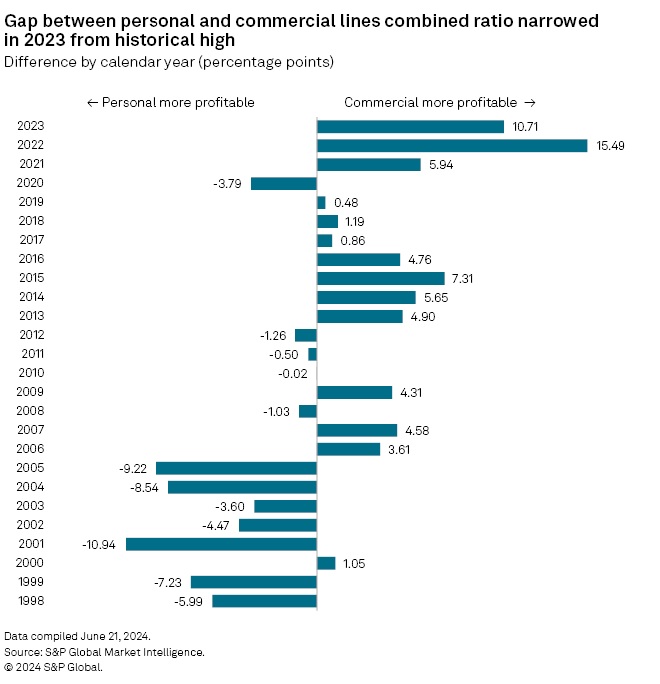

The S&P GMI report reveals clear contrasts in underwriting results for commercial vs. personal lines insurers. Except for 2020, personal lines underwriting results haven’t bested commercial lines since 2012.

In 2023, the commercial segment combined ratio was more than 15 points better than personal lines, with the difference projected to narrow to about 11 points in 2024.

Bifurcating the industry another way—by ownership structure—S&P GMI calculates a 107.9 cumulative combined ratio for the 2021-2023 period for mutuals, stock insurers that are part of mutual insurance holding company structures, and reciprocal exchanges (excluding policyholder dividends). That result was 11.3 percentage points higher than the rest of the industry.

“Mutuals tend to be more concentrated in the embattled home and auto business than stock insurers, conferring upon them the misfortune of experiencing the worst of the current cycle. But rate alone may be insufficient for them to overcome the depths of the challenges they face,” the report says.

Going forward, S&P GMI’s outlook anticipates greater market-share concentration among the largest private auto writers in the coming years, reasoning that “data, analytics and economies of scale remain critically important in a commoditized business.”

For homeowners, in contrast, S&P expects more market fragmentation as national carriers trim back exposure to loss-prone markets.

The report also includes analysis of growth in the E&S market, including premium rankings of E&S writers for homeowners and commercial property lines, drawing from a discussion of market trends included in an earlier report, The 2024 US Excess & Surplus Market.

Topics Carriers Auto Profit Loss Underwriting Personal Auto Property Casualty

Was this article valuable?

Here are more articles you may enjoy.

Florida Insurance Costs 14.5% Lower Than Without Reforms, Report Finds

Florida Insurance Costs 14.5% Lower Than Without Reforms, Report Finds  AIG’s Zaffino: Outcomes From AI Use Went From ‘Aspirational’ to ‘Beyond Expectations’

AIG’s Zaffino: Outcomes From AI Use Went From ‘Aspirational’ to ‘Beyond Expectations’  Judge Awards Applied Systems Preliminary Injunction Against Comulate

Judge Awards Applied Systems Preliminary Injunction Against Comulate  Gun Accessory Company to Pay $1.75 Million to Buffalo Supermarket Shooting Victims

Gun Accessory Company to Pay $1.75 Million to Buffalo Supermarket Shooting Victims