Top reinsurers are showing increasing – but disciplined – appetite for natural catastrophe risks as a result of rising demand, better pricing, more favorable terms and conditions, and sound investment income, according to a report published by S&P Global Ratings.

Most of the 19 largest global reinsurers rated by S&P increased their exposure to natural catastrophes during the January 2024 renewals. “We observed an average overall increase in risk exposure of 14%, although a smaller group of reinsurers continued to reduce theirs,” said the S&P report titled “Reinsurers Show Growing Appetite for Natural Catastrophe Risks.”

“Significant pricing increases, particularly in 2023, combined with reinsurers’ lower loss experience in 2023, made property catastrophe business a major contributor to the industry’s overall strong results and encouraged reinsurers to increase their exposure,” the report added.

However, if pricing weakens, S&P said, reinsurers’ appetite for raising their natural catastrophe exposures “could quickly wane.”

“For example, benign conditions in the second half of 2024 could increase pressure on reinsurers to alter terms and conditions or lower rates. We anticipate that this would prompt [reinsurers] to hold back and maintain a disciplined approach,” it continued.

The report noted that improved underwriting margins, strong investment returns, and robust capitalization “are expected to add to reinsurers’ already strong buffers against exceptional shock.”

Given the rising cost of natural catastrophes, reinsurers’ strategies have diverged during the past few years, said S&P, citing Swiss Re’s estimate of global insured losses from nat cats reaching $108 billion during 2023.

“Although this is above the long-term average for the insurance industry, higher attachment points – combined with a pattern of frequent but [mid-sized] events in 2023 – meant that a large portion of the losses fell mainly on primary insurers.”

Indeed, the report said, primary insurers bore the bulk of losses from the high frequency severe convective storms (SCS) in the U.S.

Cushioned Against Shocks

S&P warned that claims inflation, U.S. casualty claims, increasing climate variability, and financial market volatility present headwinds for the industry – but it’s current capital position is strong.

“On aggregate, we consider the reinsurance sector’s capitalization unlikely to be dented by an event so severe that it would be expected to occur only once in 100 years and would cause annual industrywide losses exceeding $250 billion,” said the S&P report. “We calculate that the sector, as a whole, would still be capitalized above the 99.99% confidence level after such an event.”

S&P forecasts combined pre-tax profits (among the 19 largest reinsurers it rates) will total $45 billion in 2024, up from the $30 billion reported in 2023. This projection would occur if:

- Investment margins remain in line with S&P’s base-case assumptions, and

- Catastrophe losses do not exceed the budgeted $19.2 billion.

“This suggests that our group has a combined buffer of about $64 billion before capital depletion would occur in a severe stress scenario. In addition, we typically expect companies to take action to protect capital in a stress scenario – for example, suspending share buybacks and other shareholder returns.”

Above Average Losses Continue

Thus far this year, insured losses are above the historical average but within reinsurers’ budgets for catastrophes, said S&P, noting that nat cats for 2024 have included SCS in the US; an earthquake in Japan; and floods in the Middle East, China, Europe, and Brazil.

“Munich Re, for example, has reported global natural catastrophe insured losses of $62 billion for the first six months of 2024 – its 10-year average is just $37 billion.”

However, primary insurers are likely to absorb a higher proportion of the losses, given reinsurers’ moves to raise attachment points, S&P said.

The report said that reinsurers’ catastrophe budgets have risen to accommodate the higher nat cat claims. “The combined budget for natural catastrophe losses in 2024 across our sample group of global reinsurers is about $19.2 billion, up from $17.1 billion in 2023 and $15.5 billion in 2022.”

S&P explained that this 2024 budget translates into an industrywide insured loss for 2024 of about $95 billion – in line with the historical 10-year average.

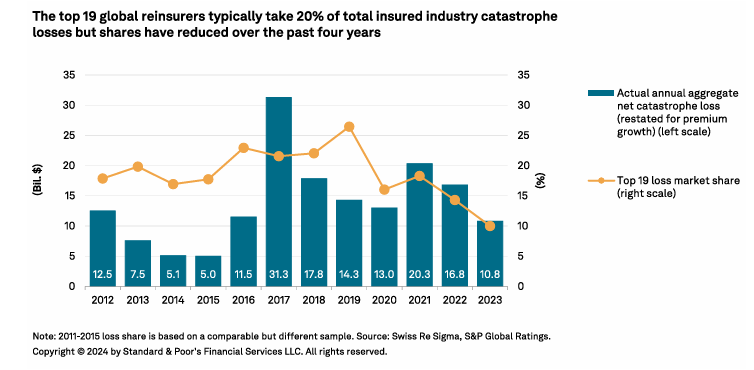

The top 19 global reinsurers typically take 20% of total insured industry catastrophe losses, the report noted.

The 19 reinsurers analyzed in the report are divided into three groups:

- Group1 of large global reinsurers: Hannover Re, Lloyd’s, Munich Re, SCOR and Swiss Re

- Group 2 of mid-sized global reinsurers: AXIS Capital Holdings Ltd., Everest Re Group, Fairfax Financial Holdings, and RenaissanceRe Holdings

- Group 3 of other reinsurance groups: Arch Capital Group, Ascot Group, Aspen Insurance Holdings, China Reinsurance (Group), Convex Re, Fidelis Insurance Holdings, Hiscox Insurance, Lancashire Holdings, Markel Group, and SiriusPoint.

Topics Catastrophe Reinsurance

Was this article valuable?

Here are more articles you may enjoy.

Court Revives Sarah Palin’s Libel Lawsuit Against New York Times

Court Revives Sarah Palin’s Libel Lawsuit Against New York Times  Dick’s Sporting Goods Reports Unauthorized Access to Information Systems

Dick’s Sporting Goods Reports Unauthorized Access to Information Systems  How One Florida Engineer Charged Others With Fraudulent Insurance Reports, Testimony

How One Florida Engineer Charged Others With Fraudulent Insurance Reports, Testimony  Audit Finds Some Florida Citizens’ Policies Over Limit, Small Use of Clearinghouse

Audit Finds Some Florida Citizens’ Policies Over Limit, Small Use of Clearinghouse