Yield-hungry insurance firms are adopting an unconventional strategy: they’re skipping mortgage-backed bonds and buying the underlying whole loans outright.

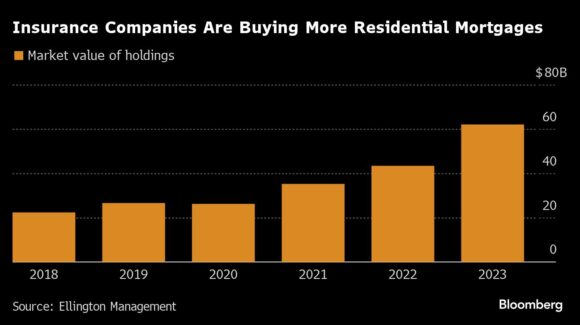

It’s a trend that’s picked up pace over the last few years. Last year alone, insurers increased their holdings of residential mortgage loans by a whopping 45%, or about $20 billion, according to an analysis by Ellington Management Group.

The loans typically don’t qualify for being bundled into bonds supported by Fannie Mae or Freddie Mac — government-backed companies that guarantee most US mortgages for investors. The borrowers are usually riskier, and investors owning mortgages directly, rather than slices of mortgage-backed bonds, means firms have to deal with arduous tasks often left to specialists. Not every firm has the size or sophistication to do that, which is why large alternative asset managers like Apollo Global Management Inc. and KKR & Co. are leading the shift.

So why bother with the hassle of owning these loans directly, rather than in securitized form? Better yields. It’s difficult to quantify exactly, but insurers with the capability to own mortgages directly could save some 35-45 basis points on the cost of securitization itself, and that’s without considering the substantial amount of capital freed up on insurance company balance sheets because of the better risk treatment, according to Ryan Singer, head of global residential investments at Balbec Capital.

“It takes getting past the legacy insurance industry’s cognitive bias against investing beyond traditional products like fixed income and commercial real estate loans,” said Douglas Dupont, Ellington’s head of insurance strategies. “But these firms have experience managing complex assets, and what they’re doing is simply looking for the best yields, adjusted for risk.”

New York-based Apollo, which acquired insurer Athene Holding in 2022, has been betting heavily on the insurance industry. Last year, Athene nearly doubled the size of its residential mortgage loan portfolio from the year before, growing it to $21.9 billion from $11.8 billion, Apollo’s full-year earnings report shows.

Others are also muscling in. Buyout giant KKR, which bought a controlling stake of insurance group Global Atlantic in 2021 and now fully owns it, increased its holdings of residential whole loans last year by nearly 20% from 2022, to $12.7 billion, according to its full-year earnings. Meanwhile, Blackstone Inc. manages money for Resolution Life and arms of giant insurers American International Group and Allstate Corp. The private equity titan’s credit and insurance business is its best-performing segment.

“This isn’t something that we started doing overnight — we first saw the opportunity here years ago and have been steadily building our capabilities,” said Chris Mellia, co-head of global asset-based finance at KKR.

Apollo and Blackstone declined to comment.

Insurers have grown interested in a variety of non-agency mortgages, but the appeal is especially strong for non-qualified mortgages. The Covid pandemic brought non-QM lending to a halt in 2020, but issuance has rebounded and now shows few signs of slowing. Demand is so strong that it’s pulling more mortgages out of the pool available for securitization. The share of all non-qualified mortgages that were securitized into RMBS fell to around 50% in 2023 from about 80% in 2021, according to a Bank of America Corp. report last month.

“Typically securitization is an attractive mode for funding assets,” said Pratik Gupta, a strategist at BofA. But now, “the non-QM market is facing competing bids from both securitizers and insurance companies which is driving a lower securitization rate.”

Insurers held over $60 billion of residential whole mortgages at the end of last year, a roughly three-fold increase from 2018, Ellington’s analysis shows.

To be sure, most investors still prefer owning mortgages through securitization — the process of bundling loans into bonds of varying risk and return. At about $8.7 trillion, the market for RMBS backed by entities like Freddie Mac and Fannie Mae — created by Congress to securitize mortgages — still dwarfs the $640 billion market for non-agency RMBS, which includes non-QM mortgages, per Wells Fargo & Co. estimates.

Administrative Muscle

Just a handful of insurance companies account for the majority of overall residential mortgage loan holdings, according to BofA. That’s because owning mortgages means dealing with physical documents like promissory notes or deeds of trust, gathering data from a variety of formats, and possibly handling the collection of payments from borrowers, among other painstaking tasks, according to Fred Matera, chief investment officer at Redwood Trust Inc., which acquires loans from originators and helps securitize or sell them.

“It takes so much work to be able to own these loans directly,” said Deva Mishra, chief executive officer of Prosperity Asset Management, which specializes in credit and niche assets. “Not everyone has the willingness and the sophistication to do it.”

Smaller insurers, or those not owned by large asset managers, are increasingly outsourcing that work. Bayview Asset Management LLC launched an insurance asset management arm solely for that purpose, tapping ex-MetLife Inc. private fixed income and alternatives head Nancy Mueller Handal to lead the effort.

Annuities, Regulations, Rates

Helping drive the shift is a combination of favorable industry risk rules and an influx of cash from annuities. Under insurance rules overseen by the National Association of Insurance Commissioners, whole loans get similar treatment as A rated corporate bonds but yield more. What’s more, a pool of mortgages in their whole loan form gets better risk treatment on insurers’ balance sheets than that same pool of mortgages when held in the form of a bond, said Dupont.

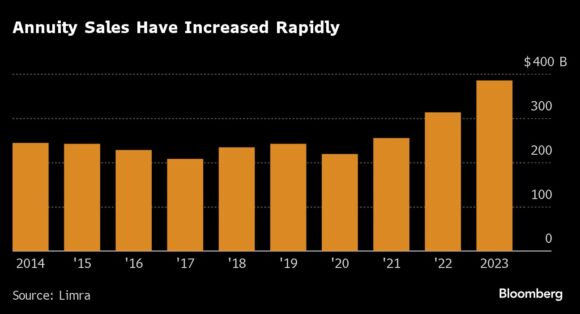

Insurers have also taken in enormous amounts of cash recently from people buying annuities. Insurers sold $385 billion in annuities last year, a more than 75% increase from 2020, according to data from Limra. Putting that cash to work in whole loans is appealing, said Bayview’s Mueller Handal, as the average life of most annuities sold today generally fits the average life of the residential loans — five or more years, roughly.

The recent regional banking crisis has also led banks to step back from buying whole loans. In recent quarters, banks which previously bought loans from Redwood now sell to it instead, said Matera. “Banks are doing the opposite of insurance companies – they’re not interested in retaining these loans in portfolio,” he added.

Meanwhile, higher interest rates have also helped boost the appeal of owning whole loans outright.

“Higher rates caused a dislocation in some of the areas that insurers usually invest, like commercial real estate and private equity,” said Matera. “At the same time, higher rates make residential loans look better to insurers, because it’s pushed yields up high enough to match what they need to pay on liabilities.”

Topics Carriers

Was this article valuable?

Here are more articles you may enjoy.

Insurance Issue Leaves Some Players Off World Baseball Classic Rosters

Insurance Issue Leaves Some Players Off World Baseball Classic Rosters  What Analysts Are Saying About the 2026 P/C Insurance Market

What Analysts Are Saying About the 2026 P/C Insurance Market  ‘Structural Shift’ Occurring in California Surplus Lines

‘Structural Shift’ Occurring in California Surplus Lines  Nine-Month 2025 Results Show P/C Underwriting Gain Skyrocketed

Nine-Month 2025 Results Show P/C Underwriting Gain Skyrocketed